- TradFi-DeFi Report

- Posts

- The 300–400 Basis Point Problem in Wealth Management and Digital Assets

The 300–400 Basis Point Problem in Wealth Management and Digital Assets

How structure erodes what investors actually keep

Antoinette Rodriguez, MBA

April 06, 2026

“Increasingly, the defining variable in wealth management is not what a portfolio earns—but how much of that return survives the structure delivering it.”

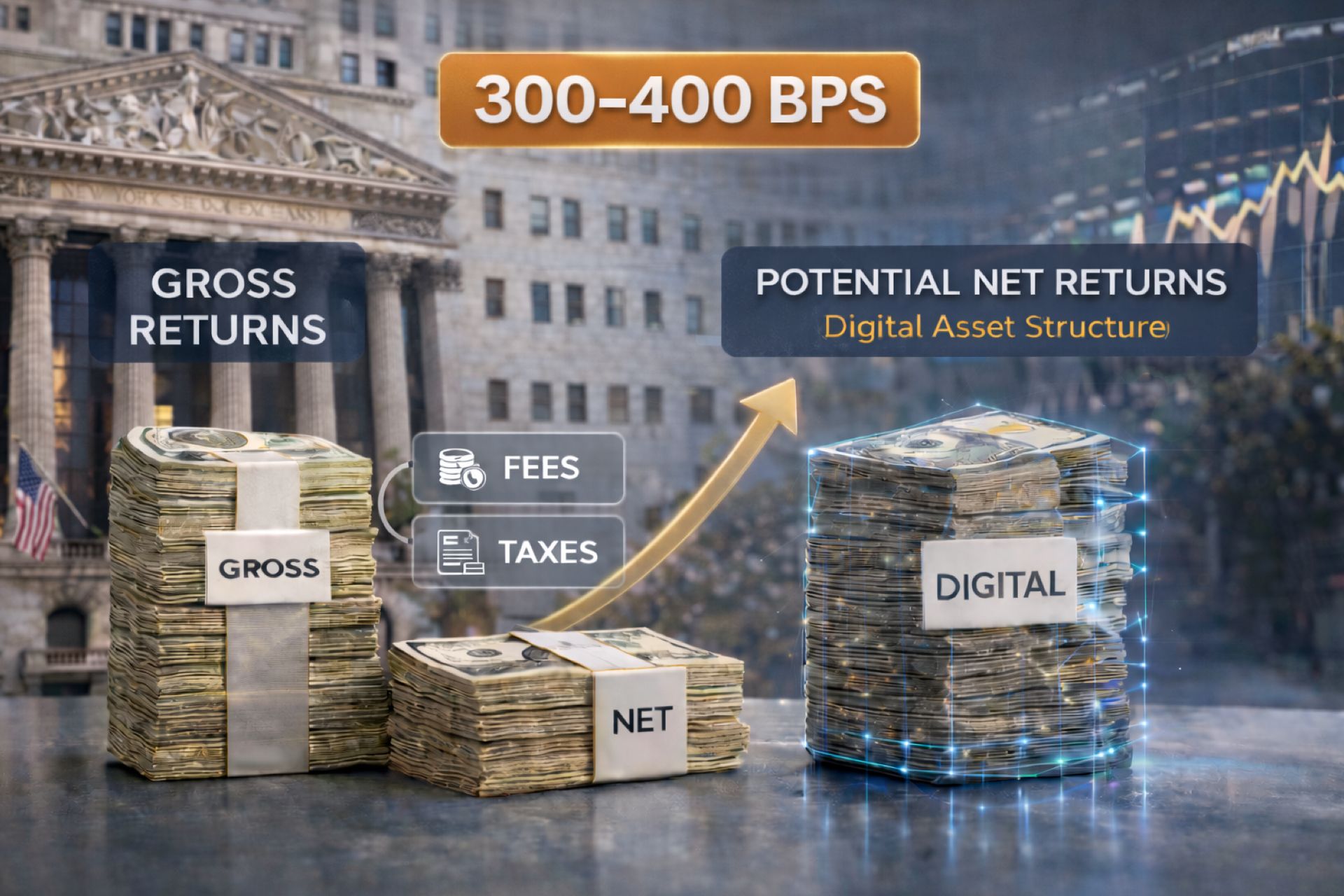

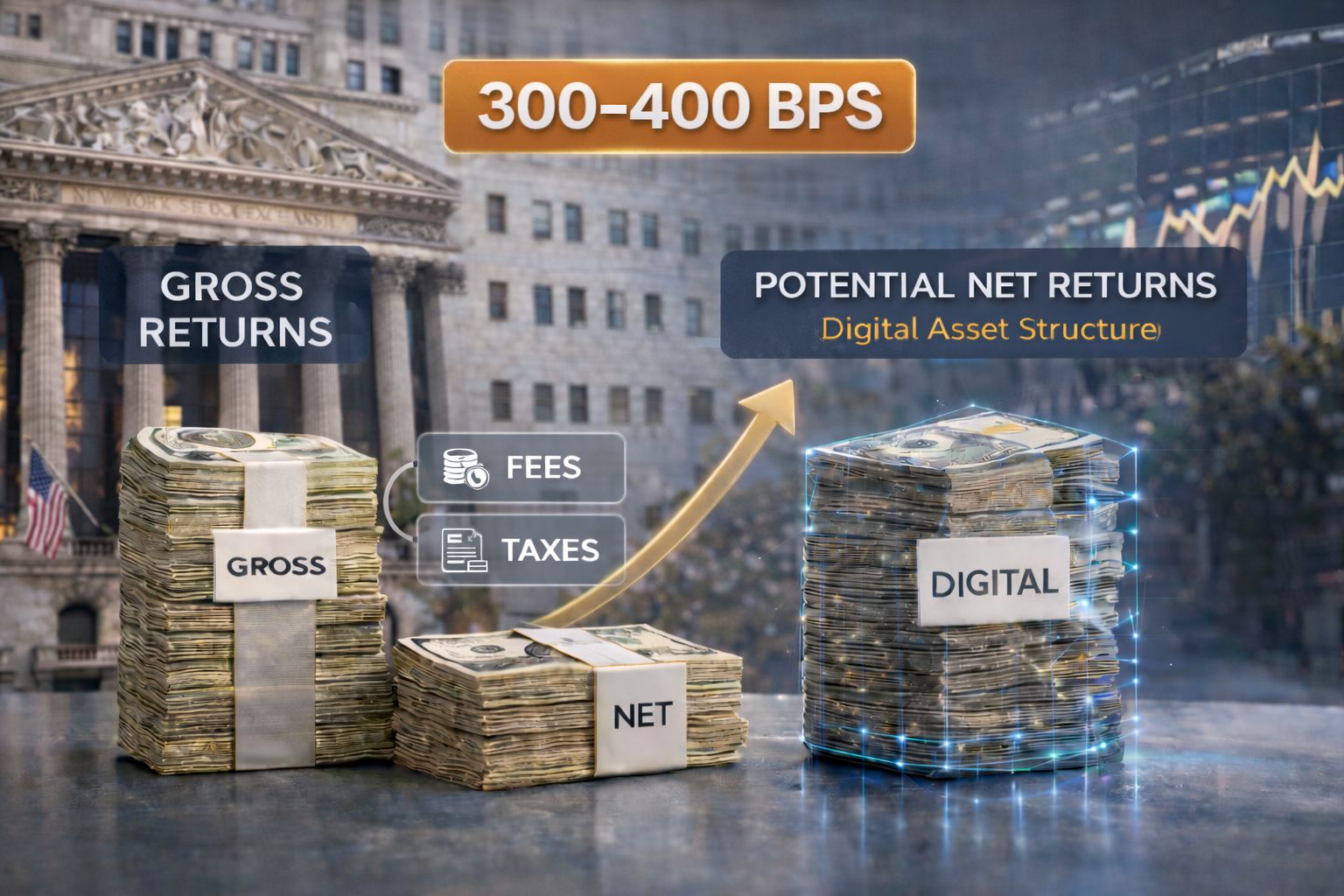

Over time, a meaningful portion of client outcomes is not driven by investment selection, but by fees, taxes, and structural inefficiencies that compound in the background. In certain high-tax, heavily intermediated portfolios, that drag can reach 300–400 basis points annually, materially eroding long-term compounding (1)(2).

The advantage is not the elimination of fees or taxes, but a shift in how and when they are incurred—often resulting in lower structural drag over time.

This is not a marginal issue. It is a structural one. And it is increasingly where the gap between gross returns and realized outcomes is either preserved—or lost.

A Structural Mismatch in Portfolio Construction

Wealth management and institutional asset management have evolved along different axes. Wealth platforms emphasize service, planning, and access, while institutional investors optimize for pre-tax performance across largely non-taxable capital pools.

That divergence creates a mismatch. Strategies designed for institutional efficiency are often inserted into taxable portfolios without fully accounting for the downstream effects of distributions, turnover, and layered fees.

The result is not just incremental drag, but compounding inefficiency—one that is often invisible in performance reporting, yet highly visible in after-tax outcomes (3).

The Hidden Layers of Intermediation

In traditional portfolio construction, intermediation is embedded at multiple levels:

– Asset management fees

– Fund-level expense ratios

– Trading and execution costs

– Custody and platform fees

Each layer may appear modest in isolation. Together, they create a cumulative impact that meaningfully alters long-term outcomes.

This is before accounting for taxation, where capital gains distributions and portfolio turnover introduce additional friction—often outside the direct control of the end investor (4).

Over time, these layers compress what investors actually retain, even in portfolios that appear to perform well on a gross basis.

Where Digital Assets Introduce Structural Change

Digital assets are often framed in terms of volatility or innovation. Less discussed—but arguably more relevant to long-term portfolio construction—is their impact on structure.

At a fundamental level, digital asset infrastructure reduces reliance on traditional intermediaries. Transactions can be executed, settled, and recorded on integrated systems, potentially compressing multiple layers of cost into a more streamlined process (5).

This does not eliminate fees. Nor does it eliminate taxes. But it can reduce the number of embedded layers through which value is extracted.

In parallel, certain digital asset structures offer greater control over when gains are realized, which can influence after-tax outcomes depending on jurisdiction and implementation (6).

The implication is not that digital assets are inherently superior—but that they introduce an alternative framework for how returns are generated, delivered, and retained.

From Gross Performance to Net Outcomes

For decades, portfolio construction has centered on optimizing returns at the asset level. Increasingly, the focus is shifting toward outcomes at the investor level.

This shift reframes the question from:

“How does the portfolio perform?”

to:

“How much of that performance does the client actually keep?”

In that context, structural efficiency becomes a primary lever—not a secondary consideration.

Even modest reductions in annual drag—whether from fees, taxes, or operational friction—can compound into meaningful differences over time.

A 300 basis point improvement in net outcomes, sustained over a decade, is not incremental. It is transformative (7).

The Institutional Direction of Travel

Large asset managers are already moving in this direction—exploring tokenization, digital infrastructure, and alternative delivery mechanisms designed to improve efficiency, transparency, and control (8)(9).

The underlying thesis is not speculative. It is operational.

If capital can move through fewer intermediaries, with greater transparency and more precise control over realization events, then the gap between gross and net outcomes can narrow.

And in an environment where returns themselves may be more constrained, that gap matters more than ever.

What This Means for Wealth Management

For advisors and wealth platforms, the implication is straightforward.

The competitive edge is no longer defined solely by access to products or allocation frameworks. It is increasingly defined by how efficiently those products are implemented—and how much value survives the journey from gross return to client outcome.

Digital assets, in this context, are not just a new asset class. They represent a potential shift in financial architecture.

One that moves the conversation from:

“What can we earn?”

to:

“What can we keep?”

References

(1) BlackRock, “Global Investment Outlook 2026,” January 15, 2026

(2) Vanguard, “The Impact of Costs on Investment Returns,” February 3, 2026

(3) Morningstar, “After-Tax Portfolio Performance and Investor Outcomes,” December 18, 2025

(4) J.P. Morgan Asset Management, “Guide to the Markets – Tax Aware Investing,” January 2026

(5) Citi Global Perspectives & Solutions, “Tokenization and the Future of Finance,” March 2026

(6) Fidelity Digital Assets, “Digital Assets and Tax Considerations for Investors,” February 12, 2026

(7) McKinsey & Company, “The Value of Financial Advice: Beyond Returns,” January 2026

(8) Goldman Sachs, “Digital Assets: Market Structure Evolution,” February 2026

(9) State Street, “The Rise of Tokenization in Institutional Portfolios,” March 5, 2026

(10) PwC, “Global Crypto Regulation and Institutional Adoption Update,” January 2026

About Antoinette (ARod) Rodriguez

Antoinette Rodriguez, MBA, is Editor-in-Chief of the TradFi–DeFi Report, a premium newsletter delivering actionable institutional insights at the intersection of traditional finance and decentralized finance.

Drawing on more than two decades of Wall Street experience—and her role as five-time Chairwoman of Financial Advisor Magazine’s Invest in Women initiative—Rodriguez provides thought leadership for institutions, wealth managers, family offices, and venture capital professionals navigating market-structure change.

Disclaimer: This newsletter provides educational content and should not be considered personalized financial advice or investment recommendations. Consult qualified and registered professionals before making decisions. While we strive for accuracy, neither Marfi Advisors, Inc. nor the authors guarantee the completeness or applicability of the information and shall not be held liable for any errors or losses arising from its use. Utilizing any strategies or services discussed is at the reader's discretion after conducting due diligence and seeking guidance. By reading or subscribing to this newsletter, you agree to these terms and acknowledge that the content is for informational purposes only and does not constitute financial advice or investment recommendations.